Benefits of Offering Retirement Plans

Attract and Retain Employees

A retirement savings plan is an essential part of your employee benefits package. Offering a retirement plan can help your company stand out among the others as workers look to change jobs. A retirement plan can also help you retain quality employees and reduce potential turnover costs.Tax Advantages

Employers can match employee contributions, which are tax deductible up to a certain limit. Employer contributions are highly appreciated by employees and can significantly increase their retirement savings over the years. Employer contributions will reduce the company’s taxable revenue and help it save on taxes while retaining employees. Company owners have the ability to not only enjoy tax advantages, but also defer income for their own retirement.Payroll Deductions

As a plan sponsor, it’s important to ensure your employees are participating in the plan and saving for their retirement. Studies show that employees are more likely to contribute to a retirement plan when payroll deductions are offered. Retirement plans can also add automated plan features, such as automatic enrollment and automatic increases to encourage more participation and increase retirement savings.Long-Term Compounding

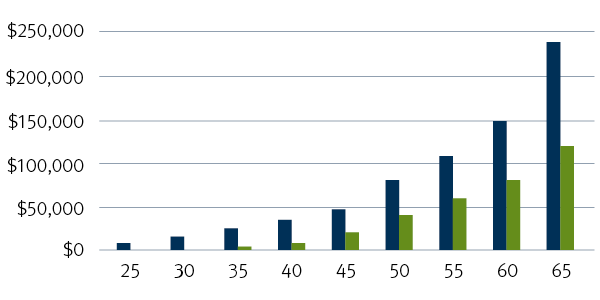

It is never too early to start planning for retirement. Investing in a retirement plan early may offer significant advantages to waiting until a later age – even if you continue to save for a greater number of years. Take for example the following scenario: |

Katie started saving $83 per month at age 21. At age 30 she stopped contributing. She left the funds in the plan until age 65. |

|

Matt started saving $83 per month at age 35. He continued to contribute the same amount for the next 30 years. |

Both Katie and Matt earned an 8% annual return, compounded monthly. Even though Katie contributed to her plan for only 10 years and Matt contributed to his plan for 31 years, Katie’s plan was worth $113,000 more than Matt’s because she started earlier. In fact, Matt contributed more money to his plan – $21,000 more. But Katie’s money had a longer time to grow.

This is a hypothetical illustration only, assuming an 8% annual return compounded monthly and is not indicative of the performance of any particular investment.

Contributions and Distributions

Some retirement plans allow employees to make contributions on an after-tax basis. While the employees do not receive tax benefits when making the contributions, their earnings will not be taxed when they make withdrawals from the plan, as long as they take the money out after they have reached age 59 ½ and at least five years have passed since the account was opened.Employer contributions are always made on a pre-tax basis. Taxes on these contributions and their earnings are deferred until withdrawals are made.

Pre-tax contributions and earnings grow and compound tax deferred as long as they remain in the plan. Once an employee separates from service or retires, he or she has four options:

- Leave the assets in the plan, if allowed

- Roll assets into a new employer’s plan

- Roll assets into an IRA

- Cash out assets

Stifel does not provide legal or tax advice. You should consult with your legal and tax advisors regarding your particular situation.

0325.7750072.1